Your wealth lives in eleven places. None of them agree.

Why did my wealth change over this period — and can I trust the number?

You can log into every account and still not answer the only question that matters: are you actually getting ahead? A net worth figure you cannot audit is not a figure you can trust.

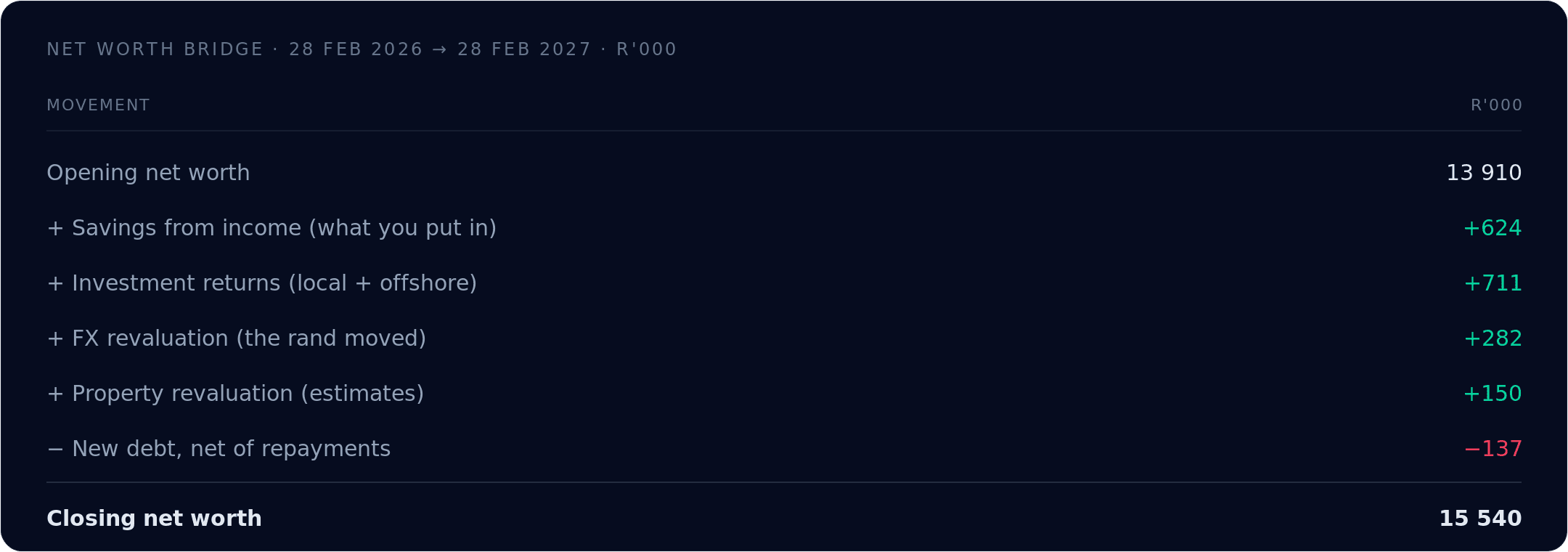

A snapshot tracker shows 13.91 becoming 15.54. Only a reconciled view shows why — and that R0.28m of it was simply the rand, which reverses the moment the currency does. Figures in R millions, illustrative.

You have a current account, a money-market account, two share-trading accounts, an offshore broker, a retirement annuity, a tax-free savings account, the bond on the house, the bond on the rental, the car finance, and a loan account in a family trust. Eleven places, give or take. Each one shows you a number when you log in. Not one of them shows you the number — the one you actually want, which is whether you are getting ahead.

So, like most people whose finances have outgrown a single bank account, you built a spreadsheet. A tab per account, a column per month, a total at the bottom. It works, mostly. Until the morning you notice the total moved in a direction that doesn't match how the year actually went, and you can't say why.

Here is a true story, lightly anonymised, from a forum of people who track their wealth more carefully than most professionals. A diligent tracker noticed his net-worth tab had quietly stopped matching his account balances. He spent the better part of a month debugging it. The cause, when he finally found it, was that he had sorted a column. A sort order had silently scrambled which balance belonged to which month, and the headline figure had been wrong ever since — confidently, precisely wrong. Nothing flagged it. The spreadsheet had no opinion about whether its own total was true.

That is the quiet problem with tracking serious money in a single list: when your finances are spread all over the place, with no coherent point where they come together, a wrong number looks exactly like a right one.

"I didn't know how psychologically dependent on it I was until it stopped working."

— an investor, on watching his account aggregator silently fail to sync for weeks

The three questions you are actually asking

Strip away the apps and the tabs, and this is what you want answered.

Where does my money actually go? Not "how much did I spend" — where did it go, in categories that mean something, with the transfers and debt repayments stripped out so the figure isn't polluted by money that simply moved from one of your pockets to another.

What is my real net worth — and is it right? One number, across every account, in rand or in dollars, that you can hand to your accountant or your spouse without a caveat.

And when it moves, was that me, the market, or the rand? This is the question no tool answers, and it is the one that matters most. Your net worth went up R1.6 million last year. How much of that did you put there by saving, how much did the market hand you, and how much was simply the rand weakening against your offshore book? Those are three completely different facts about your financial life, and a column of balances cannot tell them apart.

Why your current tools only half-answer them

There are two ways people track real wealth, and both break in the same place.

The aggregator — your bank's app, an offshore equivalent — logs into your accounts and stacks the balances. It is genuinely useful, and for a while it feels like the answer. But an aggregator shows you a pile of numbers; it cannot tell you why the pile changed, because there is nothing underneath it. Nothing has to reconcile. When a feed silently breaks — and they do — it shows you a stale balance that is indistinguishable from a live one. Users of one popular aggregator say it plainly in their public reviews:

"Obvious data errors, amounts that don't tally correctly, broken account updating which goes on for months."

— public app-store review of a leading account aggregator

The spreadsheet gives you the control the aggregator doesn't — which is exactly why careful people keep going back to it. But it has no immune system. There is no mechanism that forces the total to be checked against anything. The person who sorted his column found that out the hard way; so did the one who reflected, after years of trying every commercial tool, that "once anybody reaches a certain level of complexity, all the apps start to fall short."

Both tools fail at the same threshold: complexity. One account and one salary, and either is fine. Eleven places, two currencies, a rental, a trust — and the cracks become the whole structure.

How wrong, exactly? Wrong enough that you can't tell.

It is tempting to reach for a frightening statistic here — "spreadsheets are wrong by some neat percentage." Resist it; no honest study supports a tidy figure, and a careful reader would catch the sleight immediately. What the research actually shows is more useful, and more unsettling.

Every rigorous audit of real-world spreadsheets has reached the same conclusion: almost all of them contain errors. Across seven field audits since 1995, 94% of the 88 spreadsheets examined contained errors; in the five audits with the strongest methodologies, 91% contained errors serious in the context of the spreadsheet's use.

But the percentage is not the point. The point is the shape of those errors. Most change nothing. A minority are catastrophic. There is no comfortable middle. One transposed digit moves your total by nothing; one liability entered with the wrong sign flips your entire net worth. The error doesn't announce itself when it lands — it just quietly becomes your net worth, and stays there until something forces a reckoning.

This is the thing a single list cannot do: force a reckoning. For centuries, serious bookkeeping has used a method built precisely to make errors announce themselves — every transaction recorded in two places, so the books only balance when they are right. It is the reason a business closes its books rather than simply glancing at them. You don't need to know the method's name to feel its absence in a spreadsheet. There is no point at which your spreadsheet refuses to balance, because nothing requires it to.

Two ordinary transactions your tracker gets wrong

You don't need an exotic example to see the gap. Two payments you make every month are enough.

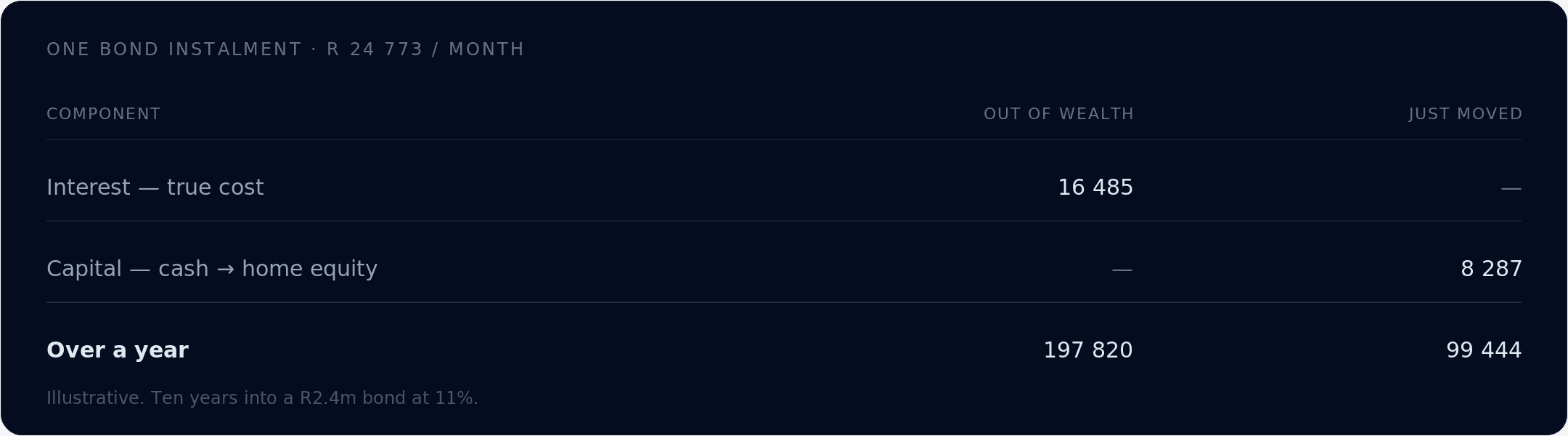

The bond payment

Say you're about ten years into a R2.4 million bond at 11%. The debit order is R24,773 a month, and a single-entry tracker logs the whole thing as "spending." It isn't. At this point in the amortisation, only R16,485 of that payment is interest — actual cost, money gone for good. The other R8,287 is capital: it didn't leave your wealth at all, it moved from one pocket (cash) into another (the equity in your home).

A tracker that calls the entire instalment an expense overstates your cost of living by nearly R100,000 a year — and understates how fast your wealth is actually growing by the same amount. Invisibly. Every year.

The credit-card settlement

The day you pay R48,000 off your credit card, most trackers record a R48,000 outflow — as if you spent R48,000 that day. You didn't. Nothing happened to your net worth on the day you paid the card: an asset (cash) fell by R48,000 and a liability (the card balance) fell by R48,000, and they cancel. The actual spending happened earlier, transaction by transaction, across the month. Single-entry tools systematically mistime card spending — which is why your "spend this month" figure lurches around for reasons that have nothing to do with how you actually lived.

Neither of these is an edge case. They are the two most common transactions in a complex household, and a list of balances gets both of them wrong.

The statement your net worth is supposed to fall out of

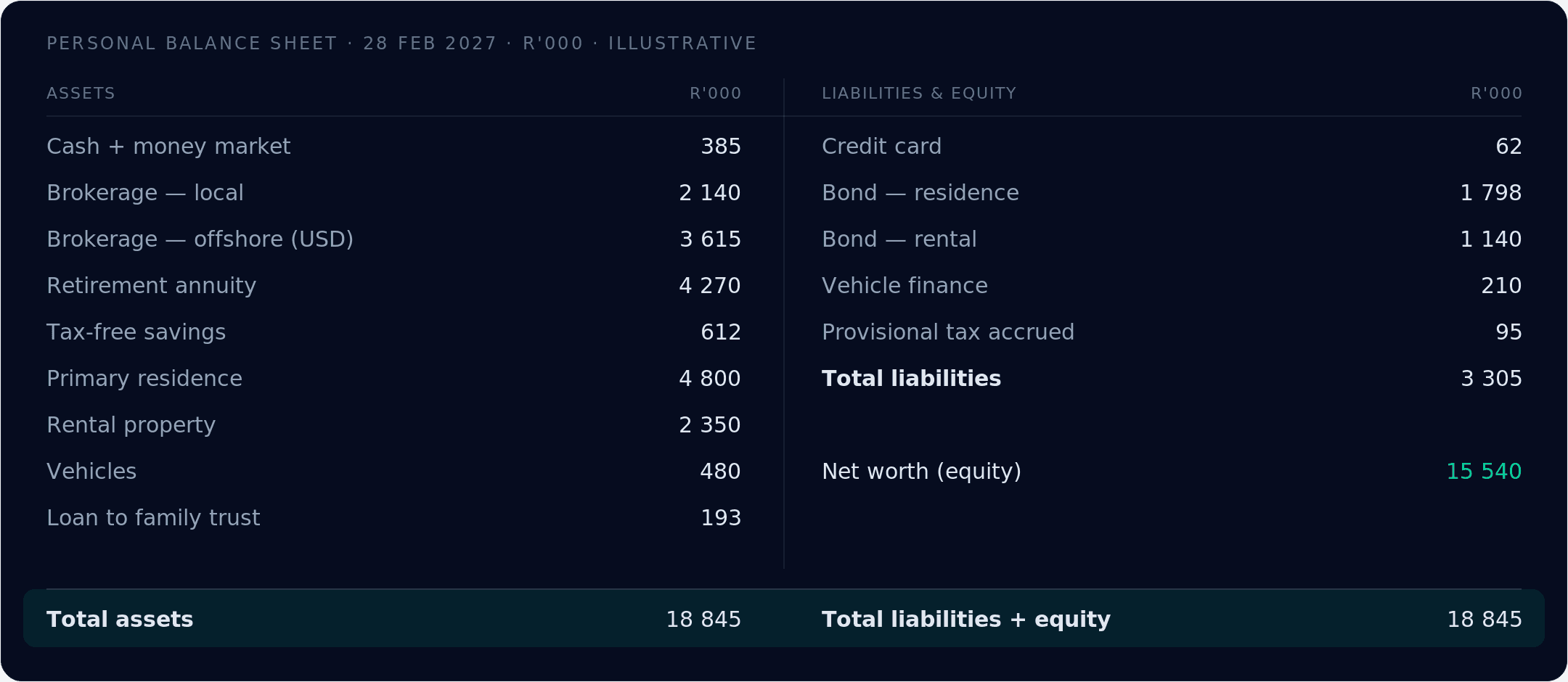

Here is the distinction that dissolves most of the confusion. Net worth is one number — the residual. It is what's left when you subtract everything you owe from everything you own. A balance sheet is the statement that number falls out of: every asset, every liability, classified and totalled, on a single date.

The sharper way to say it: a net worth figure without a balance sheet behind it is unauditable. You cannot decompose its movement. You cannot see what drove it. You cannot tell, month over month, whether it is right. It is a number you are asked to trust on faith — and faith is a strange basis for a R2 million retirement decision.

The payoff is in the last row: the two sides are forced to agree. A spreadsheet will happily show you total assets with a transposition error buried inside; a balance sheet built on proper bookkeeping cannot, because the same discipline that produces it also checks it.

Three details a careful reader will notice. The R4.27m retirement annuity is not worth R4.27m after the lump-sum tax tables — book value is not after-tax value. The offshore brokerage line moves in rand whenever the rand moves, even if the dollars sit still. And the trust loan account is an asset most spreadsheets forget entirely.

The one view that answers "was it me, or the market?"

Once the balance sheet exists and stays true over time, the question that opened this piece finally has an answer. Your net worth didn't just go from R13.9 million to R15.5 million; you can see why — line by line. (The hero chart above is exactly this bridge.)

A snapshot tool can show you 13,910 becoming 15,540. Only a proper set of books can show you that R624,000 of it was you, R711,000 was the market, and R282,000 was simply the rand — wealth that will reverse the moment the currency does. That is the difference between watching a number and understanding it.

"Isn't this overkill?"

For most people, yes — and it's worth saying so plainly, because it's true. One salary, one bank account, one credit card: a list is fine, and anyone who tells you otherwise is selling something. The honest version of the argument is not "everyone should do this." It is conditional, and the condition is complexity.

Past a certain point — more than one brokerage, any property, a second currency, a trust or company loan account; roughly, when your wealth lives in more than about five places — a single list mathematically cannot tell you the truth, for all the reasons above. It will give you a number. It just won't be able to tell you whether the number is right, or what moved it. It is less work than reconstructing two years of records in a panic the first time a tax authority, a divorce lawyer, or an estate asks you to — and far less costly than compounding a wrong number for a decade.

The other reflex is "the apps already do this." They don't. They aggregate, and aggregation is not accounting — it is the stack of balances with nothing underneath, the one that shows you a stale number with a straight face.

You may already be required to do this

There is a local twist that turns this from good practice into something closer to preparation. The South African Revenue Service already asks wealthier taxpayers to declare a statement of assets and liabilities at market value — local and foreign — as part of the annual return. Above R50 million in assets it is mandatory; for anyone with business or trade interests, a local statement applies well below that. If you have a rental, a side practice, or a provisional-tax profile, this is not hypothetical.

"Nobody audits a household" stops being true at exactly the level of wealth this piece is about. The only question is whether your declaration is assembled from books that already reconcile, or reconstructed from a year of statements in the fortnight before the deadline. The discipline that makes your net worth trustworthy to you is the same one that makes it defensible to them.

Your wealth lives in eleven places. The goal was never to admire eleven balances. It was to reconcile them into one view that adds up — and that you can prove.

See your real net worth across every account — in rand or dollar.

One reconciled view, the same number whichever way it's checked. Mintelo is the personal wealth platform built like a real one.